Wealth Strategies

Investors Rotate Towards Post-Vaccine World, Seek New Risk Tools

The outsourced CIO firm, which works with clients including those in the wealth management space, talks to this news service about asset allocation in an age where bond yields have lost some, if not all, of their value in the risk management toolkit.

Investors have been rotating portfolios to adjust to a post-vaccine world and strategies to mitigate downside risk amid volatile times have borne fruit, outsourced chief investment office business Hirtle Callaghan says.

The extraordinary market gyrations of 2020 – sharp falls in early parts of the year followed by a rebound – haven’t been easy to navigate. Volatility has spiked and, as a result of heavy central bank quantitative easing, the role that government bonds play as “ballast” is weaker because of their thin yields.

Bonds can still provide some capital protection and liquidity, but clearly more tools are required, Hirtle Callaghan’s investment chief, Mark Hamilton, told Family Wealth Report.

“Most clients will have return needs that for most of them mean taking a fair amount of exposure to equities. The [equity] market has gotten more expensive,” he said.

“The equity risk premium has stayed remarkably range-bound,” he continued. “The real issue for people is on the bond side. At these levels they are not going to drive positive returns they need.”

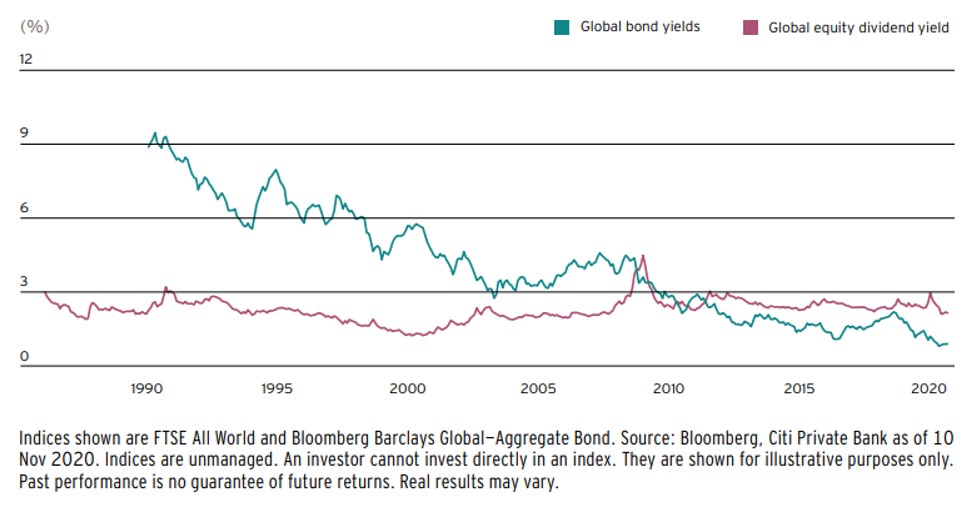

A policy of “financial repression” – transferring wealth from bond-holders to borrowers and to stoke (hopefully) low inflation – is designed to unwind the massive debts accumulated in much of the developed world. (This policy is not new: it was employed in a period after WW2.) Equity dividend yields (the reciprocal of price-earnings ratios) are now trading above bond yields and have done so for almost a decade, contrasting with the situation prior to the 2008 financial crash. (See chart below from Citi Private Bank.)

This repression does not completely push bonds off the table for

asset allocators, Hamilton said, but it does limit their scope.

“The balance it gives is there but its offsetting quality is not

there to the same degree,” he said.

A number of wealth managers have told this news service that options can be used to protect the downside to some extent, although there are risks and options carry costs, of course. Firms can sell put options (puts give holders the right to sell at a specific level) to earn some yield – although they must be careful to offset such positions if there is a sudden market fall.

“When volatility spiked as it did [in the spring] we looked at the opportunity that options allowed for us to embed some balancing in the portfolio,” Hamilton said. “The overwhelming feedback for us is that this [approach] has paid off.”

Option trading is a specialist area, but it is all of a piece of a risk management toolkit, which arguably is what smart wealth management should be all about.

“To a degree, all of what we do now is about risk management,” Hamilton said.

And this risk management task needs to be carefully explained to clients.

“Communication is a critical part of how we respond, and talk to people through this. We have had lots of calls, via the web and conference calls, with clients. For the first few months of the pandemic, we were doing these weekly,” he said.

The Hirtle Callaghan business is far from unique, of course - there is a cluster of outsourced CIOs working with family offices, UHNW individuals, foundations and charities, in most cases because the clients cannot easily justify the cost of running investments in-house. We spoke to the firm three years ago about its business model.

Private plays

There has been much industry talk and action around moving some

client money into private market areas (private equity, debt,

infrastructure, forms of real estate). In November, Preqin, the

research firm, said that the size of alternative asset classes

will expand by 60 per cent from now, reaching $17.16 trillion by

2025. That rise equates to a compound annual growth rate of 9.8

per cent.

All this begs the question: will an influx of money eventually squash yields if demand outstrips supply?

Hamilton said that the supply side of the equation remains strong, because more firms are staying private rather than entering the listed market; other firms are taking longer to go to IPO. “Firms are staying private for longer than they used to.”

“There has been an evolutionary shift there. And it is the same with private credit…there has been, since the bank regulations of 2008/9, disintermediation of traditional lenders…creating new opportunities,” he said.

What of the future?

Hamilton said equity markets are supported by the arrival of vaccines. An issue, of course, will be how fast vaccines are deployed. Meanwhile, central banks’ monetary policy remains very accommodative and a good deal of such central bank support is now priced into markets.

There is a fair amount of “pent-up” demand in the economy from people who haven’t been spending, and that money will likely drive more cyclical sectors of the economy, he said.

One feature of investor behavior is to widen out from a relatively narrow, concentrated field of Big Tech firms that did well out of the lockdown period. Hamilton said he has already seen a broadening out of the sectors that are getting investor attention. Some sector rotation is going on and was encouraged by the vaccine story.

There is also some geographic rotation. “Europe has been making up ground on the US,” he said, in terms of a catch-up and rotation effect. We tend to hold fairly broad portfolios. We did have a bias to the US coming into this year, such as towards tech, but that is broadening out,” he said.